Last Updated on December 14, 2024 by Jeysivaa | Published: February 25, 2020

In the Indian market, now everyone will be aware of SIP and does it suit them. In this article, we will see about SIP and how it works.

While Investing either in Mutual Funds or Stocks, Now the investor has the option to opt for Lump sum or SIP mode.

Are you looking for any below ?

What is SIP?

SIP refers to the Systematic Investment Plan. A Plan where the person invests regularly over a period of time.

The common SIP method will be investing a fixed amount at a fixed frequency of time.

The Frequency of Investing starts from daily, weekly, 15 days, Monthly, Quarterly.

SIP amount shall be fixed or increasing over time or decreasing over time depending on our financial goal.

How SIP differs from regular RD?

In Recurring Deposits(RD), the depositor has to deposit a fixed sum of money on a fixed day every month and that Fixed amount cannot be changed. But in SIP, there is the flexibility of variation in both the amount and the investment frequency.

To open an RD, an account to be created with a bank or post office. Likewise, to do SIP, the investor has to open a Demat account with any stockbroker.

Why do you need a SIP

SIP is a tension-free & smart way of investing money with an auto-debit option through standing instruction. It helps the investor with a disciplined approach and infuses regular saving habits within us. Through SIP, a long term wealth creation is possible.

SIP has the advantage of rupee-cost averaging when the market fluctuates. It means, with a Fixed amount, you purchase more units when the prices are low and lesser units when the price hits high. In this way.

Lump sum vs SIP – Check yourselves which suits :

- There may be a time when you invest a lump sum at the market and you earn better returns than SIP. But you have to invest at a rock-bottom level. Only a few know that level. Also, another possible outbreak when investing as lump sum when the market is high and over time market starts going down, the investor will be forced to exit with a huge loss.

- This is when SIP saves the investor, Even when the Investor invest at a market high, he does regular investments over time and rupee-cost averaging saves the investor from huge loss.

- An investor should have a high-risk appetite when opting for Lump sum.

- The Cash flow in both ways is also a major impact because lump sum takes a huge amount at a single payment whereas SIP takes a portion of the amount and regular cash flow is possible.

- For the Salaried people, SIP makes more sense because it will be a percentage/part of their take-home salary or their monthly budget and they can do the lump sum only in case of receiving an additional bonus.

- If you are new to investing, better go with the SIP route and this gives time to see the market volatility both upside and downside and yet not to go broke. SIP makes newbie more disciplined while investing.

- For the people investing for a very short term, as most people say lump sum will be a better option invested in Debt funds. Investing in debt funds through SIP for the short term gives lesser returns than lumpsum.

- Higher the Risk, Higher the return. If you want to lower the risk, Opt for SIP else lump sum may offer better returns if invested sensibly.

- In the continuously rising market, SIP gives a lesser return than the lump sum. If you know to spot the trend, go for lump sum and reap better profits.

- If you invest in ELSS Funds via SIP route, you would bee redeem your fund units one by one after 3 years where as in Lump sum deposit, it will mature as a whole after the lockin period ends.

- With SIP you don’t need a huge capital upfront whereas Lump sum needs a big capital.

- In case of going for Higher riskier funds (Equity funds), preferably go with SIP.

Facts:

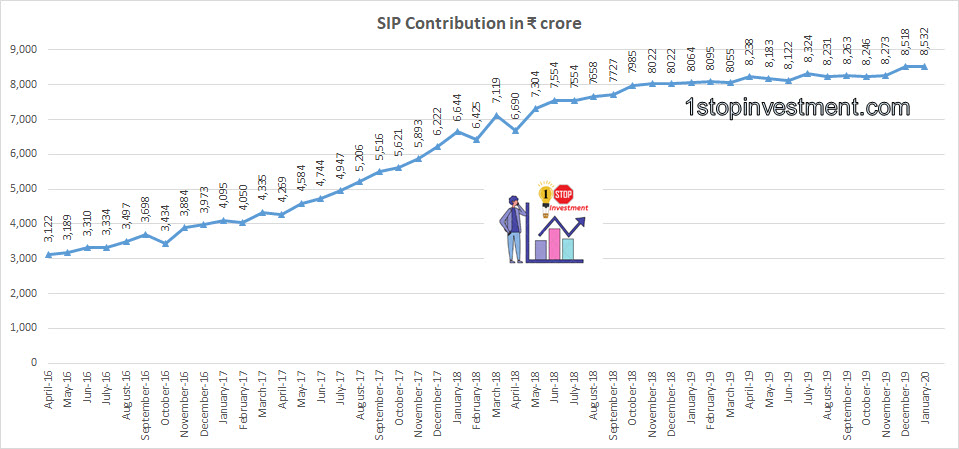

Indian Mutual Funds have currently about 3.04 crores SIP accounts through which investors regularly invest in Indian Mutual Fund schemes.

AMFI data shows that the Mutual Fund industry had added, on average, 9.81 lakhs SIP accounts each month during the FY2019-20, with an average SIP size of about ₹2,800 per SIP account.

The below graph shows the SIP Inflows every month for the past Financial years.

Source: AMFI Data

Conclusion:

Following the above points, you can now able to decide when to go for lumpsum and SIP. Yet summing up, Systematic Investment Plan depends on Fund availability, investor goal, risk profile, and duration of the investment.

Let us know in the comments, which suit you!

Please check out our SIP Calculator available here.

Also, See the Step-UP SIP Calculator tool as well.

Happy Reading Investors !!

Pingback: Latest SIP Cashflow Data – February-2020 - 1stopinvestment.com