Are you looking for any below ?

What is Debt Mutual Fund?

Debt funds are type of mutual funds where the investor’s money is invested in debt or fixed income securities like Government Bond, Corporate bond, Certificate of Fixed Deposits, debentures and money market securities with a different period. Debt funds are also referred as Income Funds or Bond Fund.

Since these funds invest in fixed income securities with very less exposure to the Equity market, debt funds offer better returns with low risk.

This is one of the better investment options whereby taking a little risk, the capital invested in appreciated better than usual Fixed deposits.

This is more suitable for moderate risk-taking investors those who already have Equity funds in their portfolio who want to diversify their portfolio and Debt Funds are the best choices that help to reduce the downside in equity funds.

Debt funds have a low-cost structure which means the expense ratio for these funds is much lesser than the Equity mutual funds.

In the Indian Debt fund Market, Interest rate movements, the CRISIL Credit rating announcement affects the NAV value of the debt fund. If the Interest rate is increased, Bond Prices rise and it makes the NAV value fall and decreases the return ultimately and vice versa.

Type of Debt Mutual Funds Instruments:

There are several types of debt Mutual funds investment. A Particular debt fund type can buy an only specific type of securities or specific maturity period securities.

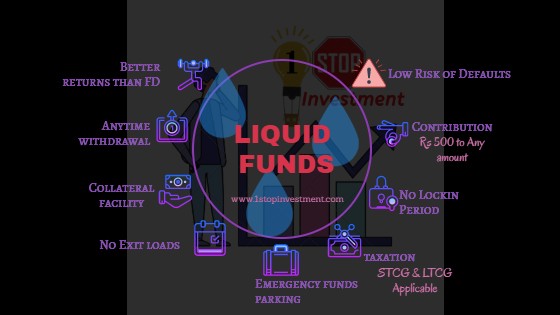

1. LIQUID FUNDS

These funds invest in debt securities where the maturity is not more than 91days or 3months. This is the least risky fund within this Debt Mutual funds instrument. Alternative to Saving bank account. This fund invests in highly liquid money market instruments and very short term securities such as Treasury Bills (T-bills), Commercial Paper (CP), Certificates Of Deposit (CD) and Collateralized Lending & Borrowing Obligations (CBLO).

2. GILT FUNDS

These funds only invest in Government securities of various tenures issued by the central and state government. This comes with various maturity period and the fund NAV have Interest rate risk and sharp fluctuations are visible in the rate cut meetings. These funds don’t carry any Credit risk or risk of default. This is the most benefitted fund in the event of falling interest rates.

3. Ultra Short term FUNDS

These funds invest in debt securities where the maturity is less than 1years. These are suited for parking short term surplus money where the horizon is between 6-12months.

4. Short term FUNDS

Short term funds invest in debt securities where the maturity is between 1-3years. These funds have very less impact even when there is change in interest rates announced or Interest-rate risk. This funds suits for low-risk appetite investors.

5. Medium-term FUNDS

These funds invest in debt securities where the maturity is between 3-5years. These funds are much more impacted when there is change in interest rates announced. Due to the larger duration of the interest rate impacts on the fund, the returns may be lower than short term funds. These are likely to be suited for risk appetite investors.

6. Long term FUNDS

These funds invest in debt securities where the maturity is beyond 5 years. These funds are much more impacted when there is change in interest rates announced. Due to the larger duration of the interest rate impacts on the fund, the returns may be lower than short term funds. These are likely to be suited for risk appetite investors.

7. Dynamic Bond FUNDS

These funds invest in debt securities with a fluctuating maturity period based on the forecast on interest rates. If the forecast is for rising interest rates, then the fund invests in short term funds and if the forecast is towards falling interest rates, the fund chooses longer maturity. These funds are slightly riskier than the term funds.

8. Fixed Maturity Plan FUNDS

These funds invest in debt plans with a fixed lock-in period. In this fund, the investor has exit loads when they withdraw before such a maturity period. These funds are similar to Fixed Deposits. The returns are not guaranteed like FD. But with Post-tax, the returns from the fund are efficient than fixed-term deposits.

9. Capital Protection Oriented Funds

As the name indicates, these funds mainly concentrate on protecting the Initial investment. CPFs invest a very small portion of equity and allow risk-averse investors to participate in Equity markets. There are no guaranteed returns or guaranteed capital protection. CPFs invest more than 80% of AUM in the AAA-rated bonds and remaining in the equity. Even if the position in the equity faces losses, the position took will be from the gains from the bonds, so the Funds are protected against the downside.

10. Credit Opportunity Funds

These funds are the riskiest type of debt mutual funds. These funds take a higher calculated risk by investing in lower-rated instruments at a lower cost. Anticipating a rise in ratings, in the hope that the lower NAV values rise in time.

*NAV means Net Asset Value

How to open Debt Mutual Fund?

All are eligible to open the debt funds and it can be opened online also.

- Identify the Debt mutual fund type which matches the investor’s goal or objective and duration and risk-taking ability.

- Investor should create an online account with the AMC (Asset Management Company). The AMC shall be selected by few base criteria’s like Exit Load, Past year returns, Average maturity value** of the fund, Funds liquidity nature, AMCs AUM value, Sharpe ratio, Fund Manager’s experience and Expense ratios***.

- After submitting KYC, the account gets active and the amount shall be invested.

- Monitor the funds regularly and it is possible to shift from one fund to another fund within the AMC by choosing Switch Options.

**Average Maturity value shows the interest rate sensitivity. If the funds have average maturity over 3-5 years deliver higher returns over the invested period. The Investment Horizon and Average maturity matches, It gives the investor to choose between funds. Average maturity doesn’t mean the lock-in period. It is an indicator of the returns in the current interest rate market.

*** The expense ratio shows how much of the AUM goes towards managing the fund. A lower expense ratio gives a higher return. Choose a fund that has a lower expense ratio and has the potential to give better performance.

*** A higher Sharpe ratio gives higher returns on every additional unit of risk taken by the investor.

Nominee

The depositor has to nominate a person who shall be entitled to payment in the unfortunate event of the death of the depositor.

How long has to Invest :

Debt Funds doesn’t have any Fixed-term lock-in period. You can invest in as long as possible and redeem it as and when required.

Exit Loads in Debt Mutual Funds

Some of the debt funds have exit loads when it is withdrawn before the no-exit load period.

Some of the funds have no exit loads also, where you can withdraw the money even on the next business day without any penalty charges.

These exit loads are lesser than the FD penalty charges in some of the funds.

Always Compare Exit loads of the funds with other funds before making any investment. A small exit load can impact much higher on the returns in a smaller period.

How Risk-Free Debt Mutual fund is :

This is more suitable for the people who are willing to take a little risk and want better returns than conventional time deposits.

However, Debt funds don’t offer any Fixed Returns but will provide market-linked returns which varies over time. When the interest rates are rising, it can have a positive impact on funds but a negative impact on bond prices vice versa when interest rates fall.

Income Tax Benefits:

No Tax deduction available under Section 80C of the Income Tax Act,1961 for any fixed deposits.

The Interest received is Taxable. Tax gets paid for the returns only when the investors redeem their money in the Debt Funds.

The Capital Tax Gain rule applies as follows :

- Short Term Capital Gains (STCG) tax if you hold your mutual fund units for less than three years

- Long-Term Capital Gains (LTCG) for investments beyond three years.

This offers better post-tax returns than usual Fixed Deposits.

However, the depositor has to declare the returns while filing Income Tax under “Income from Other Sources”.

Investment payments / Deposits in Debt Mutual Funds:

Debt Funds have the payment option either Lumpsum or SIP(Systematic Investment Plans).

Lumpsum Investment in Debt funds suits the investor when the he / she has surplus money.

SIP also possible who wants to add like RD (Recurring Deposits) which helps the investor for the rupee cost averaging.

It offers Flexibility for the Equity SIP through Systematic Transfer Plan (STP). From the lumpsum in Debt funds, a small portion (or equivalent to SIP amount) will be transferred to Equity Funds at regular intervals and spread out the risk exposure of equity lumpsum investment.

For the OLD Age Investors, who want regular periodic (monthly, quarterly, half-yearly or annually) income or regular payouts, they can opt for Systematic Withdrawal Plan (SWP).

Loan Facility

No Loan Facility available.

Conclusion

So for the people who want to increase wealth for over the period and balance their portfolio. Debt Funds is the best option to raise their capital which reduces their equity exposure, unlike Equity funds where higher volatility is expected.

Finally, Debt Funds shall be opened for goals like,

- Invest the surplus money and returns are better than normal saving account.

- Parking the Emergency Funds (6 Months Household expenses amount) here.

- Accumulating funds for Children’s education in a short duration.

- Investors who want to bring down their risk exposure in the Equity market, they can hedge some % of their capital in Debt Funds. There is a myth – “Debt funds are only for conservative investors.” But that’s not true in this case.

- Post Retirement Planning – It offers regular income with a Smaller appreciation of the capital and with Systematic Withdrawal Plan Option, the regular monthly income also possible.

Using Debts Funds, Buy some assets (It should generate positive cash flow) and never make a mistake of buying some liabilities(which depreciates than the present value) like Bike, Car, TV.

Please read the other available investing related articles here.

Please check out our SIP Calculator available here.

“Mutual Fund investments are subject to market risks, read all scheme related documents carefully.”

Well written article. Thanks. I have a serious question when it comes to debt funds. I heard that debt funds too carry bit of risk when economic faces catastrophic conditions . Ofcourse all mutual funds are having some risk . I need to agree.

And returns on these mutual funds are 1 or 2 % higher than FDs ( where you get assured returns) Also these funds are mainly for short terms so extra returns doesn’t see the magic of power of compounding. In some AMC there is also charges for MFs. Keeping all these in mind does debt funds really better than FD.

Thanks

Lokesh! Yes Debt Mutual funds are also subjected to market interest risks! Recently When most AMCs side-pocketed their exposure towardsVodafone, the short funds faces some downfall but yet they given better returns than FD.Thanks !!